Navigating The Ultra-Low Interest rate Environment

Over the past decades, global economy has been impacted by several shocks. The economic impacts of those events have been quite significant, as seen in the Global Financial Crisis, Brexit, and more recently, COVID-19. To stimulate the economy, almost all the major Central Banks implemented Quantitative easing (QE) which the central bank purchased predetermined amounts of government bonds or other financial assets in order to inject money into the economy, and in addition, the Central Banks have set interest rates to record low.

Even for Australia, in 2020, Reserve Bank of Australia (RBA) reduced the cash rate twice in March from an initial 0.75% to 0.25%, and again in November to 0.1%, record low in history.

You have heard of “record low” or “ultra-low” for many times. But have you wandered why and what’s impact on your investment?

What’s “cash rate”?

Firstly, it is important to be aware of what is “cash rate”.

Cash rate is set by the RBA for the interbank lending market-that is, where the Government, commercial banks, and other financial institutions can borrow or lend money among themselves for short-term needs. The cash rate is announced each month except January. The RBA adjusts the “cash rate” with the focus of controlling money supply and it influences and is influenced by economic conditions such as consumption, employment, inflation, and liquidity.

Thirty years ago, in January 1990, the cash rate was at a high of 17.50%. Since then, the rate has been gradually falling, to record low 0.1% in November 2020.

How does this impact your investment?

The cash rate essentially affects the cost of money. By lowering the cash rate, this lowers the interest required to be repaid on money borrowed by commercial banks in the cash market. This is then intended to encourage banks to lend more money out to consumer and institutions, thus stimulating the economy.

This has a stimulatory effect on the economy as lower cash rates generally mean you may pay less interest on money borrowed than when the cash rate is higher. This is why people might say “money has never been cheaper”.

A lower cash rate also means growth assets are revalued higher due to the potential significant returns holding these assets can deliver above the “risk-free rate”. The risk-free rate is typically considered the Australian Government bond rate.

Why is property market outperforming under low-rate environment?

Investors with large proportions of cash in their portfolio may look to re-evaluate their investment strategies and move their cash holdings into alternative investments, such as real estate. The low interest rate has contributed to the recovery of the property market where demand had built over the past months.

When interest rates are low, it generally encourages prospective home buyers to enter the market. Since home finance is more accessible, those who may have been on the fence about purchasing a property are more likely to take up a home loan and buy property.

In turn, this increase in property demand may lead to a rise in property values as stock is snapped up and homes become more difficult to obtain.

Along with the price hike, the confidence is also being built up. At the initial phase of pandemic, the Treasury estimated that COVID-19 would see cancellations of housing projects of 30%, compared with 17% during the GFC. But instead, approvals for houses have exploded to the upside. By the March quarter of 2021 dwelling approvals were annualising at 278,000. Single home approvals were even higher, with a record 136,600 approved during the year, to be 31% above the prior financial year.

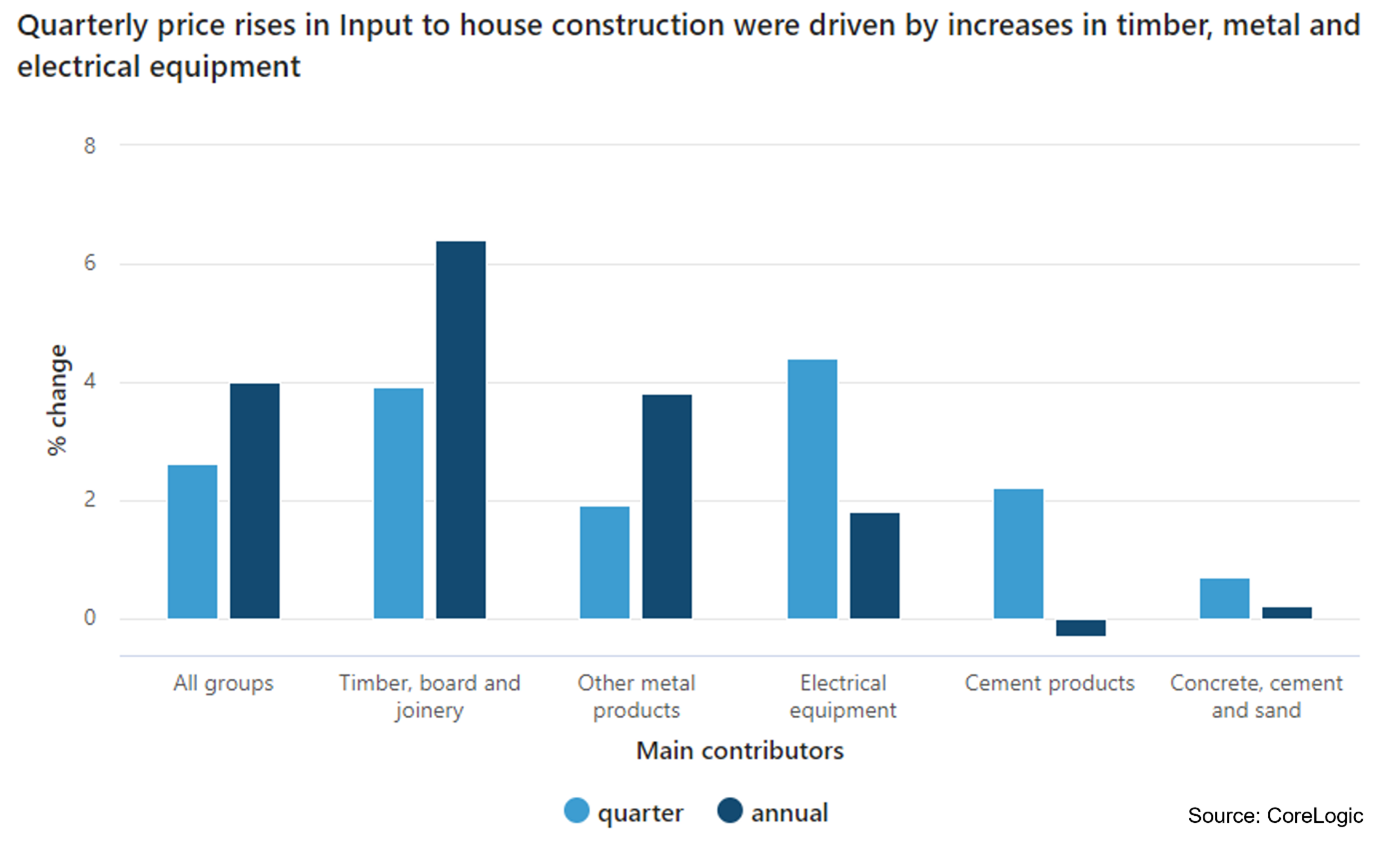

Low interest rate and QE monetary policy all contribute to the construction cost rise. According to the latest statistic by ABS, input price of timber, metal products and electrical equipment rose by 3.9%, 1.9% and 4.4% respectively, which in turn, further drive up the housing price.

From the developers’ perspectives, the funding cost is lower, which in turn increase profit margin. The project payback period and cash flow are improved due to buyers’ confidence in property marker.

The ultra-low rate has bumped up the housing price higher than pre-COVID level, and also built-up investors’ confidence. If you are also interested in property investment and looking for insight from property experts, you might consider property investment funds.

At Wharton, we offer professionally managed property investment options, and aim to provide competitive, risk-adjusted returns in this low-rate environment. Wharton Capital’s executive team has over 20 years’ experience in real estate fund management and property development finance, with funds investing across capital structure, i.e., through senior debt, mezzanine debt, preferred equity and equity. Since inception, Wharton Capital has successfully funded over 18 property projects with project value of $718 million and delivered average annual return of 10% to our investors.

If you want to learn more about Wharton’s capability, please contact us info@whartoncapital.com.au.