Market Insights - Outlook Post-Covid-19

On Monday, October 11, NSW has taken its first steps towards reopening as the state passes the 70 per cent double vaccination target for adults over 16. This is a national milestone on Australia’s road out of the pandemic and a great relief for residents and business, after three and a half months of lockdown.

Since the nation has made its first movement towards officially reopen, it’s time to think about what the world will look like after COVID-19 and what we can expect to see in domestic market once lockdown end. Here are experts’ insights and projections that we find useful for investors.

Global Economics – a Recovery Progress Comparison

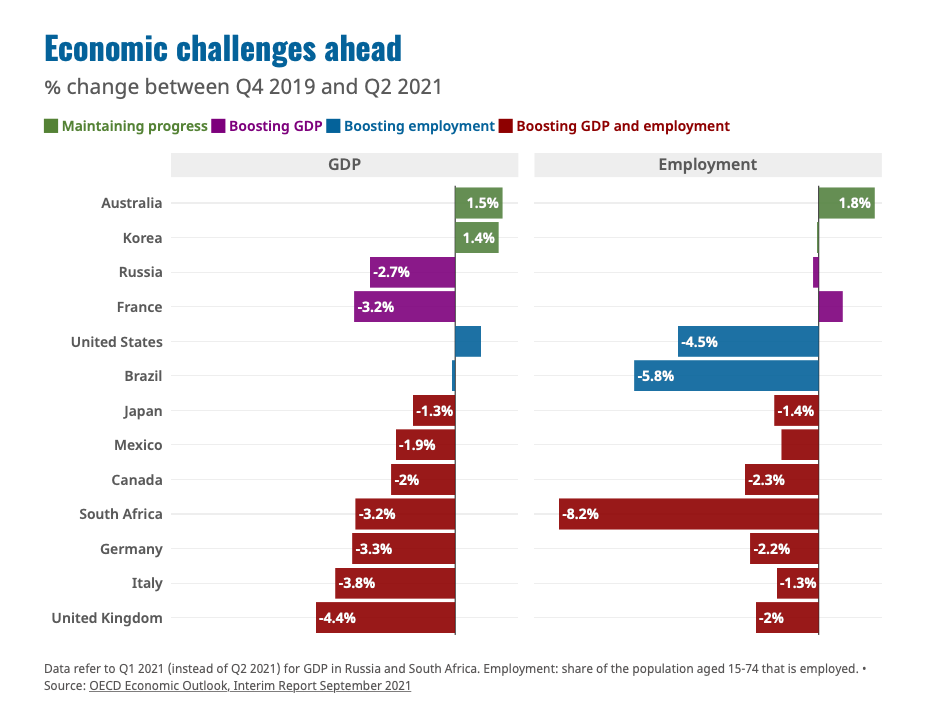

According to the latest OECD Economic Outlook released in September, the global economic recovery remains strong, helped by government and central bank support and by progress in vaccination. Data shows global GDP has now risen above its pre-pandemic level; however, the recovery worldwide remains uneven.

Australia’s GDP recovery is maintained at a healthy speed as well as employment rate, compared to other developed countries like the US, the UK and Germany, which either facing challenges of boosting GDP or boosting employment or both. It’s clear that in terms of recovery progress, Australia has outperformed most of OECD countries and make Australia one of the most investment-friendly and prudential countries for investors.

Global Economics – Real GDP & Inflation Projections

OECD Economic Outlook shows global GDP growth rates are largely bounced back in 2021 compared to 2020 to pre-covid level but is expected to slightly reduce in 2022 due to continued uncertainty due to the pandemic. Compared to other developed countries, the fluctuation of GDP growth of Australia between pre- and post-covid are less significant, proofing its well stability of economic environment.

In terms of projections of inflation globally, it’s expected to see an increased inflation in short term to 2022 among G20 countries. Developed countries like the US and UK is predicted to have around three time increases in inflation in 2022 compared to that of 2020, reached a level of over 3%. Asia-Pacific countries like China and Korea will maintain at a relevantly low inflation rate around 2%. Similarly, Australia is expected to have a 1.8% healthy inflation rate over 2022.

National Economics – Real GDP & Inflation Projections

At the onset of the pandemic, well-coordinated policies across different levels of government sought to suppress COVID-19 transmission and facilitated the reopening of the economy. The downturn in 2020 was less significant than in most other OECD countries, showing strong stability of economic environment.

Real GDP bounced back over the year to June 2021, to be above pre-pandemic levels.

Projections show annual output growth of 3.3% in 2022 and a more gradual recovery compared to the previous outbreak given it will occur in an environment with continued containment measures which are believed to restrict economic recovery.

National Economics – Low Interest Rate and Macroprudential Policy

In the short term, it is expected to see policies to keep being highly responsive to developments in economic conditions and maintain a low interest rate policy in the next few years. According to Deloitte’s veteran economist Chris Richardson, interest rate was likely to remain low for years as the current underlying inflation is remains below the RBA target and we haven’t saw a large lift in wage growth.

Underlying inflation remains below RBA target

One of the most significant consequence of low interest rate is continued strength in house prices. According to Deloitte, every 1 per cent fall in mortgage rates adds 8 per cent to measures of ‘fair value’ for house prices. This is evidenced by market changes in the past two years. Since early 2019, RBA cut its overnight cash rate target from 1.5 per cent to 0.1 per cent, driving sharp decrease in the average mortgage rates being offered to property buyers. Over the past 12 months, property prices have increased by an average 20.3 per cent across the nation and over 23 per cent Sydney, marked the highest increase in twenty years. If the interest remained at current low level, we would see a continued strength in house prices in short run.

The property boom has drawn prudential regulator’s attention. APRA has moved to take some heat out of the housing market, raising the “serviceability buffer” that banks use to assess loans. Earlier this month, APRA has written to banks telling them to increase the buffer by 0.5 percentage points, from 2.5 per cent to 3 per cent by October 31, which it says will reduce the maximum borrowing capacity for the typical borrower by around 5 per cent.

This is an expected movement. Australia has a well-established record on monitoring credit policy and macro-prudential policies, to ensuring interest rate, inflation, GDP growth, as well as property price at a sustainable level. In the long term, it is unsurprised to see RBA to embrace an array of new policy tools to adjust current high public debt and low interest rate situation. But in the short term, economist believe it’s too early to discuss about large scale uplift of cash rate as we are still putting economic recovery as priority. The RBA also reiterated in their latest statement following the September board meeting that they still expect the cash rate to remain on hold until 2024 at the earliest.

Overall, the tailwind of persistently low mortgage rates, a 30-year record high household saving ratio and improving economic conditions once lockdowns are eased will be a great support under housing demand.

The household saving to income ratio rose to 19.8%, the highest rate since June 1974. This was driven by the record fall in consumption.

In the short term, we are unlikely to see RBA change its low cash rate policy in a significant way. It is unnecessary to overly worried about the recent property boom will cause property bubble, or potential uplift of interest rate. Australian prudential regulators are carefully monitoring the market trend and will install necessary mandate to ensure market is operation in a healthy way. In the next few years, we will see macroeconomic policies to keep being highly responsive and supportive to recovery and growth in economic conditions.

References

House prices are not a bubble, says Chris Richardson

Vendors’ confidence rises as lockdowns near end

Sydney property: NSW Government missing new housing targets by 10,000 homes

Insider tips for property’s new era

https://www.afr.com/wealth/personal-finance/insider-tips-for-property-s-new-era-20210919-p58sza

$260b benefit from post-COVID-19 migrant boost

https://www.afr.com/politics/federal/260b-benefit-from-post-covid-19-migrant-boost-20210629-p5856l

Housing price growth tipped to slow to 7pc

https://www.afr.com/property/residential/housing-price-growth-tipped-to-slow-to-7pc-20210929-p58vsb

The impact of macro-prudential policies on the housing market

https://www.corelogic.com.au/news/impact-macro-prudential-policies-housing-market

APRA tightens lending rules to target property boom

Economic Survey of Australia (September 2021)

https://www.oecd.org/economy/australia-economic-snapshot/

OECD Interim Economic Outlook Sep

https://www.oecd.org/economic-outlook/

The household saving to income ratio rose to 19.8%, the highest rate since June 1974. This was driven by the record fall in consumption.